New Delhi, January 9, 2026: The Indian insurance sector, particularly health insurance, has witnessed a significant transformation in FY 2024–25. According to the IRDAI Annual Report 2024–25 (released in December 2025), the industry saw record claim settlements, improved efficiency, and a sharp rise in customer complaints — reflecting both scale and strain in one of India’s fastest-growing financial segments.

This report breaks down how insurance companies make money, the performance of the health insurance sector, and what the latest grievance data tells us about consumer experience in India’s evolving insurance ecosystem.

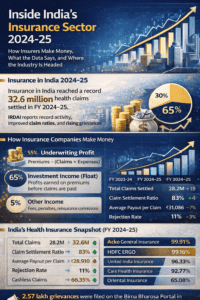

How Insurance Companies Make Money

Insurance companies primarily generate revenue from two core streams — underwriting profit and investment income.

Underwriting Profit

This refers to the difference between total premiums collected and total claims plus operating expenses.

Formula:

Underwriting Profit = Premiums – (Claims Paid + Operating Expenses)

When the “loss ratio” — the ratio of claims paid to premiums earned — gets too high, insurers lose money on their core product. In that case, efficiency in risk management becomes critical.

Investment Income (The Float)

Insurers collect premiums upfront but pay claims much later. The money held in the interim (known as the float) is invested in financial instruments such as stocks, bonds, and government securities.

For many insurers, this investment income is the key profit driver, often offsetting minor underwriting losses.

Other Income Streams

Additional revenue channels include:

-

Policy servicing fees

-

Late payment penalties

-

Reinsurance commissions (earned by sharing risk with other insurers)

Status of Healthcare Claims in India (FY 2024–25)

The IRDAI Annual Report 2024–25 reveals that India’s health insurance sector achieved record activity levels during the financial year.

| Key Metric | FY 2024–25 | FY 2023–24 | Change |

|---|---|---|---|

| Total Health Claims Settled | 32.6 million | 28.2 million | ↑ 15.6% |

| Claim Settlement Ratio (CSR) | 87% | 83% | ↑ 4% |

| Average Payout per Claim | ₹28,910 | ₹31,086 | ↓ 7% |

| Claim Rejection Rate | 8% | 11% | ↓ 3% |

| Cashless Claims | 66.35% | 62.4% | ↑ 3.95% |

The decrease in average payout per claim reflects a higher share of small-ticket retail claims, signaling deeper penetration into tier-2 and tier-3 markets.

Performance of Key Insurers

| Insurer Type | Company Name | Settlement Ratio (within 3 months) |

|---|---|---|

| Private | Acko General Insurance | 99.91% |

| Private | HDFC ERGO | 99.16% |

| Public | United India Insurance | 96.33% |

| Standalone | Care Health Insurance | 92.77% |

| Public | Oriental Insurance | 65.08% |

Private insurers continued to outperform their public sector counterparts, particularly in claim processing time and digital efficiency.

Complaints Against Insurance Companies

Despite improvements in claim settlement, the number of consumer grievances has increased sharply — largely due to rising awareness, deeper market penetration, and policy complexity.

According to the Bima Bharosa Portal (IRDAI’s grievance redressal system):

-

Total Grievances (All Insurance Types): 2.57 lakh (257,000)

-

Health & General Insurance Complaints: 1,37,361 — a 45% increase from FY 2023–24

-

Inside India’s Insurance Sector

Nature of Complaints

-

Claim-Related Issues: 69% of total grievances (≈ 88,841 cases)

-

Mis-selling: Complaints related to unfair or misleading business practices rose by 14%

-

Deductions & Disputes: Commonly over room rent sub-limits and non-medical expense exclusions

-

Delays: Complaints regarding long turnaround times (TAT) for reimbursement-based claims

The rise in grievance numbers highlights the need for more transparent communication between insurers and policyholders, especially regarding coverage, exclusions, and claim procedures.

Industry Outlook

The data paints a mixed picture — on one hand, record-high claim settlements and improved service ratios, and on the other, a growing volume of consumer complaints.

Experts suggest that as the health insurance market expands, insurers will need to invest heavily in:

-

AI-based claim automation for faster turnaround

-

Consumer education to reduce disputes

-

Regulatory compliance and ethical selling practices

With health insurance penetration in India still under 40%, the growth potential remains immense. However, the focus must shift toward sustainable underwriting and transparent customer experiences.

Data Sources

The data and insights in this article have been sourced and verified from:

Insurance Regulatory and Development Authority of India (IRDAI) Annual Report 2024–25

IRDAI Handbook of Indian Insurance Statistics

Bima Bharosa Portal (Grievance Redressal Data)

The Economic Times – 2025 CSR Rankings Report

Conclusion

India’s insurance landscape is evolving rapidly — balancing profitability, accessibility, and trust. As insurers adopt smarter underwriting and AI-led claim systems, the challenge will be to sustain growth while ensuring fairness and transparency for policyholders.

With over 32 million health claims settled and a growing base of insured citizens, FY 2024–25 marks a pivotal step toward a more mature, data-driven insurance ecosystem — one where trust becomes the new currency.

Ruchi Kumar is the associate editor at Entrepreneur News Network and TVW News India, where she leads editorial strategy, brand storytelling, and startup ecosystem coverage. With a strong focus on innovation, business, and marketing insights, he curates impactful narratives that spotlight India’s evolving entrepreneurial landscape. She has written extensively on fintech, AI and emerging startups.