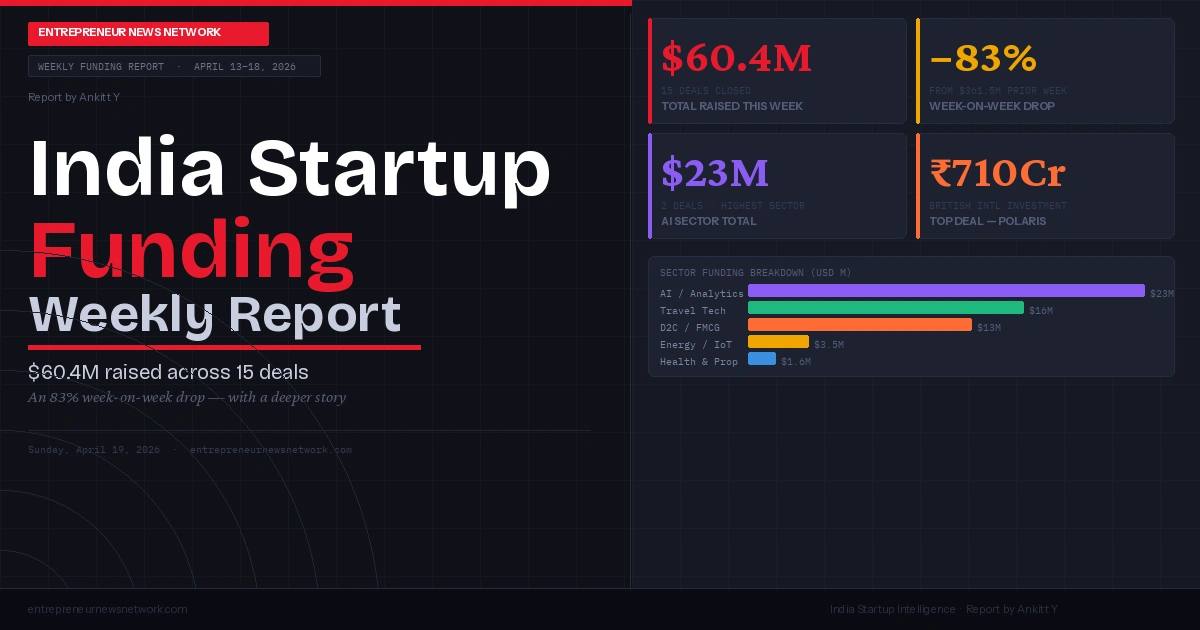

Between April 13 and 18, 2026, Indian startups closed 15 funding deals worth a combined $60.4 million — a significant week-on-week contraction of 83% compared to the $361.5 million raised across 22 deals the prior week. While the headline numbers look sobering, the week's data carries important nuance: deal quality remained high, artificial intelligence dominated by capital deployed, and infrastructure-grade companies drew international institutional attention.

The week's single largest transaction — Polaris Smart Metering's ₹710 crore debt financing from British International Investment — did not fit the conventional venture capital mould but underscored a structural shift underway in Indian startup capital markets: long-duration institutional debt from development finance institutions is increasingly funding the country's critical infrastructure buildout alongside equity-led venture rounds.

Travel tech led the equity charts. The Hosteller's ₹150 crore Series B, co-led by PROMAFT Partners and V3 Ventures, signalled continued investor appetite for organised, experience-led hospitality — a segment that rode India's post-pandemic domestic travel surge and has not looked back. The company now operates more than 75 properties across 13 states, has hosted over 20 lakh unique travellers, and is targeting 25,000 beds within 36 months.

The sharp drop should not be read in isolation. Weekly funding data in India has historically been volatile — subject to deal timing, regulatory filings, and media disclosure windows. The month of April 2026 has shown a two-speed dynamic: large institutional rounds in the first two weeks (driven by Polaris and other infrastructure deals) followed by a correction week dominated by smaller Series A activity and seed deals.

Complete Deal Breakdown: April 13–18, 2026

| Startup | Sector | Amount | Stage | Lead Investor |

|---|---|---|---|---|

| Polaris Smart Metering | Energy Infra | ₹710 Cr (~$80M) | Debt Financing | British International Investment |

| The Hosteller | Travel Tech | ₹150 Cr (~$16M) | Series B | PROMAFT Partners & V3 Ventures |

| GobbleCube | AI / Analytics | $15M | Series A | Susquehanna Venture Capital |

| HOCCO Ice Cream | D2C / FMCG | ₹100 Cr (~$10.7M) | Series C | Sauce.vc |

| TraqCheck | AI / HR Tech | $8M | Series A | IvyCap Ventures |

| Aliste Technologies | Energy / IoT | ₹30 Cr (~$3.5M) | Pre-Series A | Big Global JSC |

| Intellithink | Industrial AI | ₹17 Cr (~$2M) | Seed | Pentathlon Ventures |

| FIFTH SENSE | D2C / Fragrance | ₹6.3 Cr (~$0.75M) | Pre-Seed | OTP Ventures |

| Ivory | Brain Health | $1M | Seed | Draper Associates |

| Helium | Proptech | ₹5 Cr (~$0.6M) | Angel | Kunal Shah, Albinder Dhindsa |

| Unbound | D2C / Personal Care | ₹8 Cr (~$0.95M) | Seed | Fireside Ventures |

| Dev Milk Foods (FruBon) | D2C / Dairy | Undisclosed | Seed | Fireside Ventures |

| Smart Garage | Auto Tech | ₹2.4 Cr (~$0.28M) | Pre-Series A | Undisclosed |

| Kingdom of Chess | EdTech | ₹1.65 Cr (~$0.2M) | Angel | BeyondSeed Angel Fund |

| Cohoma Coffee | D2C / F&B | Undisclosed | Early Stage | Undisclosed |

Deal Spotlights: The Raises That Matter

Secured from British International Investment for subsidiary Hooghly Smart Metering. Funds will deploy 22 lakh smart meters in West Bengal — part of India's Advanced Metering Infrastructure (AMI) nationwide rollout.

Founded in 2014 by Pranav Dangi, The Hosteller now operates 75+ properties across 13 states, having hosted 20 lakh+ travellers. The Series B funds expansion into key travel destinations and a forthcoming travel super-app.

Founded in 2022 by Manas Gupta, Srikumar Nair, and Nitesh Jindal, GobbleCube helps consumer brands identify revenue leaks and demand gaps using AI. The platform is already serving brands across MENA and LATAM alongside India.

Backed by the Chona family — who previously sold Havmor for ₹1,020 Cr — HOCCO hit ₹530 Cr+ in FY26 net sales and is targeting ₹1,000 Cr by FY27. Production capacity will scale from 2.5 to 4 lakh litres/day.

Founded by Armaan Mehta and Jaibir Nihal Singh, TraqCheck automates hiring workflows with AI agents — Trace (background verification) and Nina (conversational sourcing). 300+ enterprise customers across India and Europe.

IoT-enabled platform for predictive maintenance and fault diagnosis using AI and proprietary sensors. Flagship product Intellivibe serves Jindal Steel, JSW Steel, and Adani. Plans to launch electrical health solutions by mid-2026.

Investor of the Week: Fireside Ventures backed two startups this week — Unbound (men's personal care) and Dev Milk Foods (FruBon dairy brand) — cementing its position as the most active investor in India's premium D2C consumer segment for April 2026.

Sector Analysis: Where the Capital Actually Went

A granular reading of this week's capital flow reveals a market in the midst of a quiet but meaningful reorientation. Three thematic threads run through the 15 deals.

Artificial intelligence captured the most capital in pure-play equity terms. GobbleCube's $15 million and TraqCheck's $8 million combined to make AI the highest-funded sector at $23 million across just two deals — an average ticket size of $11.5 million that reflects the premium investors are placing on AI-native business models with proven enterprise traction. Intellithink's ₹17 crore seed round added a third AI deal, this time in the industrial IoT application layer, a sub-segment that remains relatively undercapitalised despite strong enterprise demand from heavy industry.

E-commerce and D2C attracted the most deals but the smallest average cheque. Six deals in the consumer brand space generated only $13 million in aggregate — led by HOCCO's $10.7 million, with the remaining five deals averaging less than $500,000 each. This bifurcation within a single sector is itself a data point: institutional capital is concentrating around D2C companies with proven revenue scale and strong unit economics, while the early-stage D2C ecosystem is operating on angel and micro-VC capital. The days of institutional pre-revenue D2C bets appear to be behind us.

The seed stage suffered its sharpest correction in months. Seed funding across India dropped 86% week-on-week to just $3.3 million — from $22.9 million the previous week. This is consistent with a broader tightening at the earliest stages that has been building through Q1 2026. Investors at the seed level are demanding earlier signs of product-market fit, more defensible moats, and clearer paths to Series A. Startups at the idea or initial traction stage are encountering longer fundraising cycles and more scrutiny per meeting.

Context: India's startup ecosystem raised ₹33,000 crore (~$3.9 billion) in Q1 2026 across 380+ deals — a 26% year-on-year decline from Q1 2025, but a period marked by surgical investment precision rather than broad-based contraction. Early-stage funding, by contrast, rose 33% to $4.8 billion in FY26 — suggesting that the seed dip this week is a statistical correction, not a structural trend.

Four Trends Defining Indian VC in April 2026

British International Investment's ₹710 Cr bet on Polaris reflects a global push by development finance institutions to deploy long-duration capital into India's energy and utility modernisation programmes.

Every non-consumer deal this week had AI at its centre. GobbleCube, TraqCheck, and Intellithink are not AI-enabled products — they are AI-native business models where intelligence is the primary value delivery mechanism.

The six D2C deals this week averaged $2.2M each. Investors are writing smaller cheques and expecting earlier EBITDA paths. HOCCO is a standout precisely because it is approaching breakeven at scale — a rare combination in consumer.

Helium's ₹5 Cr angel round — backed by Kunal Shah, Albinder Dhindsa, and a cohort of operator-angels — reflects a structural shift where India's most successful founders are becoming the primary capital source for the next generation.

Looking ahead, the fundamental health indicators of the Indian ecosystem remain strong. The government's ₹10,000 crore Startup India Fund of Funds 2.0 — notified in the Gazette of India on April 13, 2026 — introduces a segmented four-track approach targeting deep tech, early-growth, manufacturing startups, and stage-agnostic categories separately. This structural upgrade to government-backed venture capital signals that public capital is maturing alongside private capital in how it thinks about the startup lifecycle.

Flipkart's reported plans to raise ₹16,000–20,000 crore ($2–2.5 billion) in a pre-IPO round from Indian and international investors — if confirmed — would represent one of the largest single capital raises by an Indian technology company in 2026, and further evidence that the late-stage IPO pipeline remains active even as early-stage activity cools.

Bottom line: This week's $60.4M is not a warning signal — it is a recalibration. The quality of deals closed (Series B travel tech, Series A AI, Series C premium D2C, DFI infrastructure debt) reflects a market that has moved decisively away from volume and toward conviction. For founders, the implication is clear: it takes longer to raise, but when capital arrives, it comes with more strategic alignment and longer holding intent.

Ruchi Kumar is the associate editor at Entrepreneur News Network and TVW News India, where she leads editorial strategy, brand storytelling, and startup ecosystem coverage. With a strong focus on innovation, business, and marketing insights, he curates impactful narratives that spotlight India’s evolving entrepreneurial landscape. She has written extensively on fintech, AI and emerging startups.