A new KPMG in India report maps how the country is moving from a data-hungry importer to a global data centre hub — and why AI is rewriting the blueprint for every server room in between.

For years, India’s relationship with data has had an odd asymmetry: the country generates roughly a fifth of the world’s data, but hosts only 2-3 percent of the world’s data centre capacity. Most of what Indians stream, swipe, and search still runs through servers sitting somewhere else.

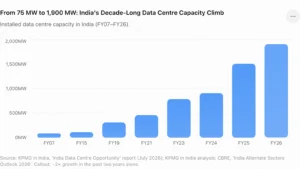

That gap is closing — fast. According to a new report from KPMG in India, “India Data Centre Opportunity: From Emerging Demand Hub to Integrated Data Centre Powerhouse” (July 2026), India’s data centre market is projected to nearly quadruple from about USD1.7 billion in FY26 to USD6.8 billion by FY30, with the country’s share of global capacity expected to almost double to around 5 percent in the same window. Installed capacity, which has more than tripled since FY19 to reach roughly 1.9 GW today, has a development pipeline set to add another 4.5 GW over the next five years.

Behind that growth is a number that tends to stop people mid-scroll: over USD120 billion in investment commitments already made by hyperscalers, Indian conglomerates, and global and domestic data centre operators for the Indian market, per KPMG’s analysis.

Why the world is suddenly looking at India’s server rooms

KPMG’s report lays out a fairly simple economic case for why global capital is turning toward India. On construction costs, Mumbai ranks as the world’s second most cost-effective city for building a data centre — roughly half of what it costs in Singapore or Tokyo. On power, India’s average electricity cost of USD7.5–8/kWh is among the cheapest globally, backed by a power grid that hit 500 GW of installed capacity in mid-2025, about half of it renewable — meeting India’s COP26 clean-energy commitments ahead of schedule. And on talent, the report notes that Indian software engineers earn roughly a quarter of what their counterparts in Japan or Australia do, even as India’s AI talent pool is forecast to more than double by 2027.

Put together, KPMG frames India as sitting at a rare intersection: enormous latent demand (it already produces a fifth of the world’s data), and some of the most favourable unit economics anywhere for building the infrastructure to house it.

AI isn’t just adding demand — it’s redesigning the data centre itself

Perhaps the more interesting story in the report isn’t how much capacity India is adding, but what kind. KPMG’s analysis describes this as a “full-scale redesign, not an incremental upgrade” — data centres are shifting from centralised, CPU-led, air-cooled facilities to distributed, GPU-driven, liquid-cooled architectures built for far denser, far hungrier workloads.

The scale of that shift shows up in the numbers: rack densities that used to top out around 8-12 kW are heading toward 50-60 kW for AI workloads, with some specialised AI/HPC racks pushing 120-150 kW. Cooling is moving from basic air conditioning to direct-to-chip liquid cooling and immersion systems. And crucially, the report flags a structural constraint that will shape the next decade of construction: only 25-30 percent of India’s existing data centre capacity can realistically be retrofitted to meet AI workload standards. Most of this has to be built new.

By FY30, KPMG projects AI workloads will account for roughly 55 percent of total Indian data centre capacity, rising to about 65 percent by FY35 — with the AI-driven slice of the market alone growing from under USD2 billion today to an estimated USD17 billion by FY35.

The bigger opportunity might not be the data centres — it’s everything around them

For builders, suppliers, and investors, KPMG’s report makes the case that the more durable opportunity sits in the ecosystem feeding India’s data centre boom. The firm estimates the cumulative data centre construction and infrastructure value chain — design and construction, power systems, cooling, networking, and security — at roughly USD30 billion by FY30, scaling to USD90 billion by FY35.

The report breaks this down by segment, and the localisation picture is uneven — some categories are already dominated by Indian players, others remain heavily import-dependent:

- Design and construction (~USD27 billion by FY35): Already has strong Indian EPC presence, but specialised design capability for large AI-ready facilities is still concentrated among international firms — which KPMG flags as a clear whitespace for Indian engineering firms to move into.

- Power infrastructure inside the DC (~USD18 billion): Highly concentrated, with the top three global players controlling 65-70 percent of the UPS and critical power market — though manufacturing is gradually shifting to India.

- Cooling infrastructure (~USD24 billion): One of the fastest-evolving and most import-heavy categories — KPMG notes liquid cooling technology today is “almost entirely imported,” leaving room for Indian players to partner with specialist global firms.

- Power infrastructure outside the DC (~USD12 billion), network and connectivity (~USD5 billion), and security (~USD5 billion) round out the value chain, each with its own mix of local strength and import dependence.

KPMG’s broader argument: building a competitive domestic supply chain is becoming just as strategically important to India’s data centre ambitions as attracting the hyperscalers and capital in the first place.

The policy tailwind — and why New Delhi is treating servers like national infrastructure

The report devotes real attention to the regulatory story, and it’s a telling one. Since 2022, data centres above 5 MW of IT load have carried “infrastructure status” in India — unlocking longer-tenure debt (15-20 years, at rates several points lower than before) and access to infrastructure debt funds. The 2023 Digital Personal Data Protection (DPDP) Act tightened rules around domestic data storage. The IndiaAI Mission has provisioned more than 34,000 GPUs at heavily subsidised rates. And most recently, the Union Budget 2026-27 introduced a tax holiday running all the way to 2047 for qualifying foreign cloud service providers operating through India-based, Indian-owned data centre infrastructure.

KPMG frames this as more than industrial policy — it’s a national security argument. With systems like Aadhaar (now processing over 200 crore face-authentication transactions), UPI, and the National Health Stack all depending on sovereign, low-latency compute, the report argues that India’s control over its own data centre capacity has become inseparable from its control over its own digital governance.

The economic ripple effects, KPMG estimates, are substantial: the data centre ecosystem today generates a 2.5-3.0x economic multiplier through ancillary industries and employment, a figure the report expects to climb to 3-4x as domestic manufacturing and services deepen. On jobs specifically, the report projects employment across the data centre value chain growing from roughly 1 million today to 9 million over the next decade.

The takeaway

Strip away the acronyms — DPDP, PUE, WUE, EPC — and KPMG’s report is telling a fairly clear story: India spent the last decade becoming one of the world’s biggest consumers of data. The next decade, the firm argues, is about whether it becomes one of the world’s biggest hosts of it — and whether the companies building the racks, the cooling systems, and the power infrastructure to make that possible are Indian ones or imported ones.

With over USD120 billion already committed and a construction value chain KPMG pegs at USD90 billion by FY35, that question is no longer hypothetical. It’s under construction.

This article is based on findings from KPMG in India’s report, “India Data Centre Opportunity: From Emerging Demand Hub to Integrated Data Centre Powerhouse,” published July 2026. All data, figures, and projections cited are sourced from KPMG in India’s analysis unless otherwise noted within the report. Full report available at kpmg.com/in.

Asia’s Startup Funding Roundup: 10 Deals, $92.9 Million, and an AI Funding Wave (July 5-10, 2026)

Ruchi Kumar is the associate editor at Entrepreneur News Network and TVW News India, where she leads editorial strategy, brand storytelling, and startup ecosystem coverage. With a strong focus on innovation, business, and marketing insights, he curates impactful narratives that spotlight India’s evolving entrepreneurial landscape. She has written extensively on fintech, AI and emerging startups.