In India, booking a plumber, a massage therapist, or a deep-cleaning crew through an app has become routine enough that the market built around it is now worth roughly $60 billion, with three well-funded startups burning real money to fight over the fastest-growing slice of it. In most of Southeast Asia, the equivalent transaction still usually starts with a text message to a neighbour, a recommendation in a building’s WhatsApp group, or a name scrawled on a piece of paper taped to a lift. The question being asked across the region’s venture capital circles is whether India’s model can be exported. The data suggests something more specific than a simple yes or no: India’s own home services industry is still mid-fight, concentrated in a handful of cities, burning significant cash to grow, and — as of today — showing no real outbound intent toward Southeast Asia at all.

Part 1: The Current State of India’s Home Services Industry

A $60 Billion Market That’s Still 90% Informal

India’s home services market — spanning cleaning, pest control, appliance repair, handyman work, painting, and renovation — carries a total addressable market of roughly ₹5,100–5,210 billion, or approximately $60 billion, in FY2025, according to Redseer Research figures cited in Urban Company’s IPO prospectus. That’s projected to grow at a 10–11% compound annual rate to around $100 billion by FY2030.

What’s notable is how little of that market has actually gone digital. The industry remains 90.5% unorganized as of FY2025 — that share is expected to fall only to 87.9% by FY2030, a glacial pace of formalization. Offline organized players (local contractors, agencies, and franchises that aren’t app-based) hold an 8.7% share, growing to 10.8% by FY2030. Online full-stack platforms — the Urban Companys and Snabbits of the world — currently hold just 0.8% of the total market, projected to roughly double to 1.3% by FY2030. The online segment specifically is valued at $41–43 billion and growing at a much faster 18–22% CAGR, which is the number investors are actually betting on, even though it’s a sliver of the total pie today.

The Market Leader: Urban Company’s Position

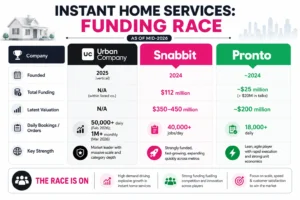

Urban Company, founded in 2014 as UrbanClap, has emerged as the clear category leader and is now estimated to hold more than 60% market share within the organized, online segment of India’s home services industry. The company listed on Indian stock exchanges in September 2025, with its IPO oversubscribed nearly 104 times and shares debuting at a 56–57% premium over the issue price.

Urban Company’s scale numbers, drawn from its own disclosures and IPO filings: more than 40,000 registered professionals globally, over 25 training centres, presence across roughly 59 cities in India plus UAE, Singapore, and Saudi Arabia, and a serviceable addressable market within India’s top 200 cities valued at $21 billion (drawn from 53 million households). Its standalone net sales reached ₹281.72 crore for March 2026 alone, up nearly 39% year-on-year — but the company has also posted three consecutive quarterly net losses since its IPO, including a ₹161.2 crore loss in Q4 FY26, driven almost entirely by aggressive investment in its instant-services vertical, InstaHelp.

The City Map: Still Overwhelmingly a Metro Game

Despite a decade of operating history, Urban Company’s own CEO has been candid that the company remains, in his words, “by and large… a metro phenomenon.” The company has a presence in roughly 40 Tier-2 cities, but its real density sits in India’s top 10 metros — Delhi NCR, Mumbai, Bengaluru, Chennai, Hyderabad, Pune, Kolkata, Ahmedabad, and a handful of others — where household income, dual-income families, and smartphone-led digital adoption are highest.

The newer instant-services category is, if anything, more geographically concentrated than the broader Urban Company business. Snabbit, the leading challenger, operates live in just five cities: Delhi NCR, Mumbai, and Bengaluru as its core markets, with a smaller presence in Pune and Hyderabad. Pronto has followed a similarly narrow-but-deep strategy, prioritizing density within existing cities over geographic sprawl. Industry executives quoted in Indian business media expect this category to remain concentrated in India’s top 10–15 cities for the foreseeable future, with only “selective expansion” into Tier-2 markets over time — a sign that even within India, the instant home-services model hasn’t been proven outside the country’s wealthiest, densest urban clusters.

The Competitive Battlefield: Three-Way Cash War

The instant home services category — Urban Company calls its version InstaHelp; competitors are Snabbit and Pronto — has become one of the most heavily funded battlegrounds in Indian consumer tech over the past year, mirroring the early, subsidy-heavy years of quick commerce.

Snabbit, founded in 2024 by former Zepto executive Aayush Agarwal, has been the most aggressive fundraiser. It raised a $56 million Series D round in April 2026, co-led by Susquehanna Venture Capital, Mirae Asset Venture Investments, and Bertelsmann India Investments, valuing the company at roughly $350–450 million — up from $180 million just six months earlier. Total funding raised stands at approximately $112 million. The company says it processes more than 40,000 jobs daily across a network of over 15,000 workers, and claims to be running at an annualized revenue rate of $35–40 million, while also claiming it has cut its burn per order by 50% over six months — though it remains loss-making.

Pronto has taken a similar high-velocity-funding path, raising approximately $25 million and reportedly in talks for another $20 million round led by investor Lachy Groom at a roughly $200 million valuation. The company scaled from around 1,000 to over 18,000 daily bookings in just seven months.

Urban Company’s InstaHelp, despite entering the category more recently than its venture-backed rivals, has used its existing scale to take the lead: InstaHelp crossed 1 million monthly bookings by March 2026 and over 50,000 daily bookings by February 2026 — ahead of both Snabbit and Pronto on raw volume — but at a steep cost. The unit was losing ₹447 (about $4.70) per order in Q4 FY26, up 17% from ₹381 the previous quarter, with an adjusted EBITDA loss of ₹119 crore against revenue of just ₹9 crore in the same quarter — a loss large enough to erase the ₹22 crore in profit generated by every other Urban Company category combined.

Consolidation Is Already a Familiar Story in This Market

This isn’t India’s first home-services cash war, and history offers a sobering precedent for how these things tend to end. Earlier players Housejoy and Zimmber both competed directly with early Urban Company; Housejoy ultimately shut down and Zimmber faded into irrelevance, while smaller city-specific players were either acquired or pivoted away from the category entirely. Industry retrospectives are direct about why Urban Company survived where others didn’t: not because it was first or cheapest, but because it had the capital to outlast underfunded rivals while investing in supply-side quality (training, vetting, tools) rather than just demand-side growth (discounts, marketing). That same dynamic — well-capitalized incumbent versus venture-fueled new entrants burning cash for share — is now replaying in the InstaHelp-vs-Snabbit-vs-Pronto fight, and India’s own market history suggests consolidation, not permanent three-way coexistence, is the more likely outcome.

Part 2: Who Actually Wants to Leave India?

This is the more surprising finding in the data: based on current public disclosures, no major Indian home services player has announced concrete plans to expand into Southeast Asia. Urban Company — the only Indian home services company with a genuine multi-country track record — has built out a four-market international footprint (UAE, Singapore, Saudi Arabia, alongside India), but that footprint excludes Indonesia, Vietnam, Thailand, and the Philippines, the four largest population centres in Southeast Asia and the markets that would actually define a “Southeast Asia strategy.”

More tellingly, Urban Company has already tried — and abandoned — two international markets: Australia and the United States, both shut down after the company found local consumer behaviour fundamentally incompatible with its operating model. Founder Abhiraj Singh Bhal has described a cultural split: Gulf and Singaporean consumers showed a “do it for me” mindset similar to urban India’s, while Australian and American consumers leaned “do-it-yourself” and were often unwilling to stay home while a professional worked inside it — undermining a structural assumption the business depends on. Notably, Urban Company has not stated similar plans to test Vietnam, Indonesia, the Philippines, or Thailand, despite having operated in nearby Singapore for several years.

Snabbit and Pronto — India’s most aggressively funded challengers — are, based on all available reporting, entirely focused on deepening density within their existing five or so Indian cities rather than any international expansion; none of the funding announcements, founder interviews, or investor commentary reviewed mention Southeast Asia as a target market. The capital currently flowing into this category is being spent exclusively on out-competing rivals inside India, not on geographic expansion.

This absence of outbound ambition is itself informative. It suggests that, as of mid-2026, India’s home services operators view their own domestic market — at $60 billion TAM and only 1.3% online penetration projected even by 2030 — as offering more attractive, lower-risk growth than the comparatively tiny, more fragmented Southeast Asian opportunity.

Part 3: The Size Mismatch With Southeast Asia

Southeast Asia’s formal online home services market was valued at just $137.51 million in 2024, according to UnivDatos Market Insights, with projected growth at a 14.25% CAGR through 2033. Put plainly: India’s online-only home services segment, at $41–43 billion, is roughly 300 times larger than Southeast Asia’s entire formal home services market combined.

The region’s category is currently served by a fragmented set of domestic players rather than any single dominant platform: Singapore-based Helpling (which has moved into institutional facilities-management contracts), Vietnam’s bTaskee, Malaysia’s ServisHero, Indonesia’s OKHOME, and regional super-app Grab, which has been folding home-adjacent services like solar panel and EV charger installation into its existing GoLife platform — suggesting Southeast Asia’s path to formalization may run through super-apps bundling the category in, rather than a dedicated unicorn entering from outside.

The Bottom Line

India’s home services industry, on its own data, is not a finished, exportable playbook — it’s a market still actively consolidating, still 90% informal, still geographically concentrated in roughly 10–15 cities, and still burning hundreds of crores annually to determine which of three well-capitalized players wins the instant-services category domestically. Until that internal contest resolves and InstaHelp-style economics prove sustainable at home, there is no real evidence — in funding rounds, founder statements, or market entries — that any Indian operator is preparing to test the playbook on Southeast Asia’s far smaller, more fragmented market.

Sources: Urban Company DRHP/RHP filings; Redseer Research; HDFC TRU; UnivDatos Market Insights; Inc42; TechCrunch; Bloomberg; Business Standard; MediaNama; TechStory; BusinessToday; Tracxn; Wikipedia; Limitless Builders.

India Climbs to 94th in UN SDG Index 2026, but Hunger Remains a Major Challenge

Ruchi Kumar is the associate editor at Entrepreneur News Network and TVW News India, where she leads editorial strategy, brand storytelling, and startup ecosystem coverage. With a strong focus on innovation, business, and marketing insights, he curates impactful narratives that spotlight India’s evolving entrepreneurial landscape. She has written extensively on fintech, AI and emerging startups.