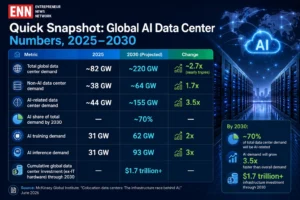

A new McKinsey Global Institute (MGI) report, “Colocation data centers: The infrastructure race behind AI,” lays out a striking number: global data center demand could almost triple between 2025 and 2030 — from about 82 gigawatts (GW) to roughly 220 GW. AI alone is expected to drive nearly 70% of that growth, with AI-related demand rising 3.5 times from 44 GW to 155 GW by 2030. Cumulative global investment in data center infrastructure (excluding IT hardware like GPUs and servers) could top $1.7 trillion by the end of the decade.

That’s the global backdrop. But where does India fit into this race — and what does it mean for Indian businesses, investors, and policymakers? This article breaks down McKinsey’s key findings and maps them against India’s own colocation and AI infrastructure story, which is growing faster than almost any other market in Asia-Pacific.

The Global Picture: What McKinsey Found

McKinsey’s analysis benchmarks the “levelized cost” of building and running a 100-megawatt, liquid-cooled AI colocation data center — essentially the minimum price per megawatt-hour needed to make such a project viable — across five major hubs: Northern Virginia (US), Beijing/Shanghai (China), London (UK), Northern Sweden, and Singapore. A few headline takeaways:

- China’s eastern hubs are cheapest to build in, at roughly $200 per MWh, while London is the most expensive, at nearly $380 per MWh.

- Electricity is the single biggest cost driver, accounting for almost 30% of the cost variation across countries. Power prices in London are 1.9 times higher than in China’s major demand centers.

- Power and cooling equipment account for another ~30% of cost differences — hot climates like Singapore need heavier cooling investment, while markets like the UK and Sweden face higher equipment costs due to stricter redundancy standards.

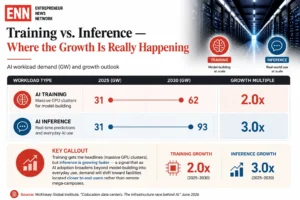

- Chip access changes the math entirely. US-designed AI accelerators remain far more compute-efficient (measured in PFLOPS per megawatt) than China’s leading domestic chips, which are estimated to be roughly 10x less efficient. That means China’s low infrastructure costs can be wiped out once GPU efficiency is factored in — a critical insight for any country trying to compete on “cheap land and power” alone.

- Speed, not just cost, wins deals. Equipment lead times (generators, chillers, transformers, switchgear) have more than doubled since 2019, and grid connection queues can now stretch beyond four years — in some markets, up to a decade. McKinsey estimates up to 50% of global data center capacity due online in 2026 could be delayed by permitting and grid bottlenecks.

- Colocation economics vary by business model more than geography. Retail colocation earns $200–380 per kW/month with 20–25% IRRs, while wholesale/hyperscaler leases earn $150–200 per kW/month with 13–18% IRRs.

This last point matters enormously for India, because India’s colocation market is built almost entirely on winning exactly these two dynamics: cost-competitive power and land, and increasingly, speed of delivery.

Where India Stands in the Global Infrastructure Race

India didn’t make McKinsey’s five-country cost comparison, but its trajectory tells a parallel — and in some ways more explosive — story.

India’s capacity is growing faster than almost any market McKinsey studied

- India closed 2025 with colocation capacity of roughly 1.5–1.7 GW across seven metro hubs (Mumbai, Chennai, Delhi-NCR, Bengaluru, Hyderabad, Kolkata, Pune), according to CBRE and Cushman & Wakefield data.

- Capacity is projected to reach 1.7–2.0 GW by the end of 2026, an annual growth rate of roughly 30% — supported by an estimated 500 MW of fresh supply in 2026 alone, up from 440 MW added in 2025 (itself a 160% jump over 2024).

- Longer-term forecasts put India at 4–5 GW by 2030, and one market-research estimate (Mordor Intelligence) projects installed IT load climbing from 5,450 MW in 2026 to over 15,000 MW by 2031 — a 22.8% CAGR.

For context: McKinsey’s global demand forecast implies the world moves from 82 GW to 220 GW by 2030, a roughly 2.7x increase. India’s own capacity growth trajectory (1.7 GW to 4–5 GW) implies a similar or steeper multiple — evidence that India is scaling in step with, or ahead of, the global curve, even from a smaller base.

The investment numbers are now genuinely large

- Cumulative investment commitments into India’s data center sector reached $126 billion by end-2025, with $56.4 billion committed in 2025 alone. CBRE projects this could cross $180 billion by the end of 2026 — a roughly 45% year-on-year jump.

- Vestian estimates India’s data center market was worth about $10 billion in 2025 and will more than double to $22 billion by 2030.

- Foreign institutional investors have supplied nearly 80% of total capital inflow into Indian data centers between 2020 and 2024, underlining how India has become a preferred APAC destination for global infrastructure capital — directly echoing McKinsey’s point that AI data centers are now competing for capital the way traditional infrastructure (power, ports, telecom) once did.

India’s real edge: construction cost, not necessarily power cost

McKinsey’s global analysis shows electricity price is the number one driver of levelized cost differences. India’s story is a bit different — its structural advantage today is construction cost, not the cheapest power in Asia.

- Data center construction costs in India run at roughly $6–7 million per MW, notably lower than in mature APAC markets such as Singapore and Japan, and well below the capex intensity McKinsey models for Northern Virginia, London, or Sweden.

- On power, India is improving but not yet best-in-class: large hyperscale self-builds are locking in 15-year renewable power purchase agreements (PPAs) to bring costs below ₹4 per kWh, competitive with — though not clearly cheaper than — China’s benchmark levelized costs in McKinsey’s model.

- India added a record 44.5 GW of renewable capacity in 2025, nearly double the previous year, which is increasingly being funneled into data center PPAs — a domestic version of the “supply-advantaged market” strategy McKinsey highlights for regions like Sweden.

The GPU dependency problem applies to India too

McKinsey’s finding that chip efficiency can “flip the economics” of a cheap-power market is directly relevant to India. India currently has no domestic advanced AI chip design or fabrication capability at the frontier level — it remains dependent on US-origin accelerators (Nvidia, AMD) routed through global supply chains, the same chips McKinsey flags as the most compute-efficient but also the most export-controlled and supply-constrained. This means India’s colocation cost advantage on land, labor, and construction can only translate into competitive AI compute economics if operators can reliably source top-tier GPUs — a bottleneck India shares with much of the world outside the US and China.

Speed and policy are becoming India’s real differentiators

McKinsey stresses that markets winning investment today combine “connectivity, demand, and speed of execution” — and increasingly, alignment with national priorities (what the report calls “sovereign AI”). India has moved deliberately on this front:

- The Union Budget 2026–27 introduced a long-term tax holiday running until 2047 for foreign cloud providers using India-based infrastructure, provided they operate through an Indian reseller — a direct incentive for hyperscalers to build or lease locally rather than serve India from offshore.

- States including Telangana, Maharashtra, Tamil Nadu, Andhra Pradesh, and Uttar Pradesh have rolled out dedicated data center policies and are expected to lead capital inflows in 2026.

- A draft National Data Center Policy and data-localization mandates under the Digital Personal Data Protection Act are pushing global cloud players — Microsoft, Google, AWS, Amazon — toward India-based capacity rather than cross-border hosting.

- Major anchor deals underline the momentum: AdaniConneX’s 400 MW Chennai campus (with 200 MW of integrated renewables), a $15 billion Google–Adani cloud alliance for Bengaluru, Delhi-NCR, and Mumbai, Microsoft’s 50 MW Hyderabad expansion, and Yotta’s $200 million-funded 250 MW Greater Noida project combining solar and battery storage.

Where the capacity is concentrated — and where it’s spreading

- Mumbai remains the dominant hub, with roughly 49–50% of India’s operational data center capacity, thanks to submarine cable landings and financial-sector demand.

- Chennai follows with about 18%, benefiting from multiple subsea cable connections.

- Bengaluru, Hyderabad, and Pune are emerging as secondary hubs, and Mordor Intelligence projects Bengaluru will see the fastest capacity growth of any Indian city (23.8% CAGR), driven by low renewable tariffs and hyperscale GPU projects.

- Tier-II cities — Ahmedabad, Visakhapatnam, Kochi, Jaipur, Patna, Bhopal, Lucknow, Guwahati, Bhubaneswar — are gaining traction as operators chase lower land costs, state incentives, and demand for lower-latency edge infrastructure tied to 5G rollout.

Reading McKinsey’s Findings Through an Indian Lens

Putting the global report and India’s numbers side by side, a few strategic implications stand out:

- India competes on capex, not electricity price — for now. McKinsey shows utilities account for nearly 30% of global cost variation. India’s $6–7 million/MW construction cost is a genuine edge, but sustained competitiveness will depend on locking in cheaper, firmer renewable power at scale — something the 44.5 GW of new 2025 renewable capacity is starting to enable.

- Speed of delivery matters as much as cost. McKinsey warns that permitting delays and multi-year grid connection queues could delay up to half of global 2026 capacity. India’s tax incentives, state-level fast-tracking, and standardized campus designs (like AdaniConneX’s and Yotta’s renewable-integrated builds) are direct responses to this global bottleneck — and a source of competitive advantage if India can keep execution fast.

- GPU access remains the swing factor. Just as chip efficiency can erase China’s cost advantage in McKinsey’s model, it can just as easily cap India’s upside. Without secure, large-scale access to frontier accelerators, India’s low-cost colocation infrastructure risks becoming a home for inference and enterprise workloads rather than frontier AI training — a meaningful but smaller slice of the $1.7 trillion opportunity.

- Business model will decide who profits. McKinsey’s finding that retail colocation (20–25% IRR) outperforms wholesale hyperscaler leases (13–18% IRR) is a live question for Indian operators like CtrlS, Sify, STT GDC, Nxtra (Airtel), and Yotta as they decide how much capacity to preleased to hyperscalers versus retain for higher-margin enterprise and BFSI clients — a segment McKinsey notes typically demands higher redundancy and commands a premium.

- Sovereign AI is now a real policy lever. McKinsey highlights Europe’s growing embrace of “sovereign AI” investment (citing SoftBank’s €75 billion France commitment). India’s data-localization mandates and the 2047 tax holiday for India-hosted cloud infrastructure are the domestic equivalent — an explicit bet that policy alignment, not just cost, will determine where the next wave of AI infrastructure capital lands.

The Bottom Line

McKinsey’s report frames AI data centers as one of the defining infrastructure investment stories of this decade, with total capacity almost tripling globally by 2030 and $1.7 trillion in cumulative capex at stake. India isn’t one of the five markets McKinsey benchmarked directly, but its own numbers — capacity nearly tripling from 1.7 GW to 4–5 GW, investment commitments crossing $180 billion in 2026, and construction costs among the lowest in Asia-Pacific — suggest it’s running its own version of the same race, just a few years behind the US and China in absolute scale.

The determining factors will be familiar from McKinsey’s global analysis: securing reliable, competitively priced power; cutting the time it takes to connect new capacity to the grid; and — the hardest lever for any country outside the US and China to pull — securing consistent access to the advanced AI chips that ultimately decide whether cheap infrastructure translates into cheap compute.

Data and analysis referenced from McKinsey Global Institute’s “Colocation data centers: The infrastructure race behind AI” (June 2026), part of the MGI report “Catalyzing Competitiveness: Where Investment Happens and Why,” alongside industry data from CBRE, Cushman & Wakefield, Vestian, JLL, and Mordor Intelligence.

Ruchi Kumar is the associate editor at Entrepreneur News Network and TVW News India, where she leads editorial strategy, brand storytelling, and startup ecosystem coverage. With a strong focus on innovation, business, and marketing insights, he curates impactful narratives that spotlight India’s evolving entrepreneurial landscape. She has written extensively on fintech, AI and emerging startups.