India’s Global Capability Center (GCC) ecosystem has crossed another milestone in FY2026, and the numbers tell a story that goes well beyond scale. According to the newly released Zinnov-Nasscom “GCC Value Orbit: From Delivery Engine to Enterprise Nerve Centre” report, India is now home to 2,117 GCCs, generating $98.4 billion in revenue and employing 2.36 million professionals — cementing its position as the world’s largest and most mature GCC hub.

But the headline numbers only tell half the story. The report’s real finding is structural: the role of India’s GCCs has changed faster than most enterprises have redesigned their operating models around it. Below is a complete, numbers-first walkthrough of what the report says.

The Core Numbers: From $61.4Bn to $98.4Bn in Five Years

The report frames FY2026 as the culmination of a five-year growth run:

- GCC revenue climbed from $61.4 billion in FY2021 to $98.4 billion in FY2026 — a jump of roughly 60% in dollar terms and 32% growth in the number of centers.

- The GCC workforce grew from 1.7 million in FY2021 to 2.36 million in FY2026.

- In just five years, India added more than 500 new GCCs and over 1,000 new GCC units.

- Only a few years ago, industry projections pegged India’s GCC market at crossing $100 billion by 2030. FY2026 data shows the ecosystem is now tracking well ahead of that curve, with the $98.4 billion mark nearly reached four years early.

This puts to rest any narrative that GCC growth in India is slowing — the ecosystem has actually accelerated relative to earlier five-year projections from the same Zinnov-Nasscom report series.

The Real Signal: 96% of New GCCs Skip the “Crawl-Walk-Run” Model

This is arguably the most important data point in the entire report. Historically, GCCs in India followed a predictable maturity arc — starting as cost-arbitrage delivery centers and earning strategic mandates over years (the “crawl-walk-run” model).

The FY2026 data shows that model is now the exception, not the rule:

- 96% of GCCs established after FY2021 launched with product or portfolio ownership mandates from day one — bypassing the traditional crawl-walk-run evolution entirely.

- Nearly half of all GCCs set up since FY2021 were built with AI as a core design focus from inception, not bolted on later.

- The report’s own framing captures this shift precisely: “Maturity that took a decade is now a design choice made on day one.”

In other words, the compression of the maturity timeline isn’t a side effect of the AI boom — it is the defining structural shift of this report cycle.

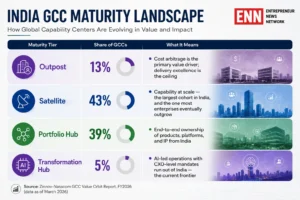

The Zinnov GCC Maturity Framework: Where India’s GCCs Stand

The report applies Zinnov’s proprietary GCC Maturity Framework — the industry-standard classification used across the entire GCC Landscape in India report series — to the FY2026 dataset. It splits India’s 2,117 GCCs into four tiers:

Two data points stand out here:

- 46% of India’s GCCs now sit in the Portfolio Hub or Transformation Hub category, up from 42% in FY2021 — a meaningful jump in genuine strategic ownership, not just headcount.

- The report identifies a “compression curve”: 27% of GCCs now reach Portfolio Hub status within just five years of setup — a timeline that used to take a decade.

- Looking ahead, the report projects that close to three-fourths (~75%) of India’s GCCs could reach Hub status by FY2030.

AI Is No Longer a Project Inside the GCC — It Is the GCC

AI capability is the connective tissue running through every section of the FY2026 report:

- India is now the #1 AI hiring market globally, according to the report.

- The country’s GCC ecosystem has a talent base of over 250,000 AI/ML professionals — more than double the ~120,000 AI/ML professionals reported just two editions earlier.

- More than 1,200 GCCs in India have embedded AI and machine learning capabilities into their operations.

- These capabilities are backed by over 250 dedicated AI/ML Centres of Excellence (CoEs).

- The report notes a shift in the nature of AI conversations inside GCCs: from “what AI can do” to “how to govern it and make it economically viable at scale.” AI has moved from experimentation into being deployed across products, internal operations, and customer-facing offerings simultaneously.

Zinnov CEO Pari Natarajan summarized the opportunity this way: India holds one of the largest and fastest-growing pools of AI and digital talent in the world, and the centers that build on this — by investing in frontier capabilities and deepening links between talent, academia, and industry — stand to benefit the most from India’s continued rise.

Nasscom President Rajesh Nambiar echoed the same shift, noting that the transition from scale to value is now well underway, with AI acting as the catalyst as GCCs increasingly take ownership of global products, platforms, and business outcomes — effectively becoming a strategic nerve centre for their enterprises rather than a support function.

Who’s Setting Up GCCs in India — The Ownership Breakdown

The FY2026 dataset breaks down India’s 2,117 GCCs by the type of parent organization:

- 506 Forbes Global 2000 companies operate a GCC in India — a strong signal that GCCs have become a default part of enterprise strategy for the world’s largest companies, not a niche cost play.

- 583 mid-market GCCs now form a growing, distinct cohort — enterprises below the Fortune/Forbes 2000 scale that are increasingly setting up India centers.

- 504 GCCs are private equity (PE)-backed — showing that PE-owned portfolio companies are now a significant driver of India’s GCC expansion, not just multinational corporates.

Together these categories underline how broad-based India’s GCC growth has become — spanning mega-cap enterprises, mid-market companies, and PE-backed businesses alike.

City-Wise Breakdown: Bengaluru Still Leads, Hyderabad Is the Fastest Riser

While Bengaluru remains the anchor of India’s GCC ecosystem, the FY2026 report data (as also reported around the report’s release) shows a notable shift in city-level share:

- Bengaluru holds the largest share of India’s GCC network at 29%, still the top hub thanks to its large talent ecosystem, established startup network, and leadership hiring pipeline.

- Hyderabad’s share expanded from 12% (FY24) to 14% (FY26E) — driven by rising traction in engineering, semiconductor, and AI-focused GCC operations, aided by proactive state-level policy engagement.

- Other established hubs — Pune, Chennai, and the NCR region — continue to anchor the remainder of India’s top GCC cities, each carrying distinct sectoral strengths (e.g., BFSI and automotive depth in Pune/Mumbai; engineering, healthcare, and renewable energy diversification in NCR/Chennai).

- Beyond the top five metros, the report and related industry commentary point to growing enterprise interest in Tier II cities as companies look for lower operating costs and access to emerging talent pools — supported by stronger state government engagement.

Zinnov’s research underpinning the report draws on real estate data across India’s top 8 GCC cities, giving the location-strategy findings a granular, city-by-city foundation.

The Research Behind the Report

The report’s credibility rests on the scale and depth of the underlying research, which the Zinnov-Nasscom teams describe as follows:

- 200+ primary interviews with GCC heads, CTOs, and CHROs across India.

- Analysis of 1 million+ GCC job postings across India to map talent and skill demand.

- Real estate data across India’s top 8 GCC cities.

- Zinnov’s continuously updated Global Capability Center tracking database, maintained for over two decades and covering every major GCC hub from Bengaluru to Hyderabad, Pune, Chennai, and NCR.

- The findings draw on Zinnov’s operational track record of 220+ GCC setups and transformations, and its role in placing 250,000+ professionals into GCCs globally — meaning the benchmarks in the report are grounded in real implementation data, not modeled estimates.

The Three Structural Shifts the Report Highlights

The FY2026 “GCC Value Orbit” report distills its findings into three structural shifts that it argues most enterprises have not yet caught up with:

- Centers built for delivery are increasingly holding global ownership. GCCs originally set up to execute are now being handed authority over products, platforms, and business outcomes.

- Maturity that took a decade is now a design choice made on day one. New GCCs are being architected with product/portfolio mandates and AI-first design from the outset, rather than earning that maturity over years.

- The ecosystem is ahead. The org chart is behind. Enterprise operating models — reporting lines, decision rights, and global org structures — have not kept pace with how much authority India-based GCC leaders now actually hold.

What’s Next: The Road to FY2030

Based on the trajectory captured in this and prior editions of the Zinnov-Nasscom report series:

- India’s GCC market size is projected to reach $99–105 billion by 2030, with some estimates suggesting the market could approach $110 billion within five years.

- GCC headcount is expected to cross 2.5 million professionals.

- Close to three-fourths of India’s GCCs could achieve Portfolio Hub or Transformation Hub maturity by FY2030, compared to 46% today.

- Continued expansion into Tier II and Tier III cities — such as Coimbatore, Ahmedabad, Indore, and Bhubaneswar — is expected to diversify the geographic footprint beyond the current top hubs.

FAQs: India’s GCC Landscape 2026

How many GCCs are there in India in 2026?

2,117 GCCs, spread across 3,728 GCC units — a 32% increase since FY2021.

What is the India GCC market size in 2026?

$98.4 billion in revenue, employing 2.36 million professionals, as of FY2026.

Is India the largest GCC market in the world?

Yes — the report positions India as the world’s largest and fastest-growing GCC hub, ranked #1 globally for AI hiring.

Which city has the most GCCs in India?

Bengaluru, with a 29% share of India’s GCC network, followed by Hyderabad at 14% (up from 12% in FY2024).

How many companies from the Forbes Global 2000 have GCCs in India?

506 Forbes Global 2000 companies operate a GCC in India, alongside 583 mid-market GCCs and 504 PE-backed centers.

Credits & Source

All data, statistics, and findings referenced in this article are drawn from the Zinnov-Nasscom India GCC Landscape 2026 Report — “The GCC Value Orbit: From Delivery Engine to Enterprise Nerve Centre” (FY2026 edition), co-published by Nasscom and Zinnov, with K Raheja Corp as Industry Partner. Additional context has been drawn from related public commentary on the report’s release, including statements from Pari Natarajan (CEO, Zinnov) and Rajesh Nambiar (President, Nasscom).

Full report and methodology: zinnov.com/centers-of-excellence/zinnov-nasscom-india-gcc-landscape-2026-report

This article is an independent summary and analysis for informational purposes. All rights to the original data and report belong to Zinnov and Nasscom.

Ruchi Kumar is the associate editor at Entrepreneur News Network and TVW News India, where she leads editorial strategy, brand storytelling, and startup ecosystem coverage. With a strong focus on innovation, business, and marketing insights, he curates impactful narratives that spotlight India’s evolving entrepreneurial landscape. She has written extensively on fintech, AI and emerging startups.