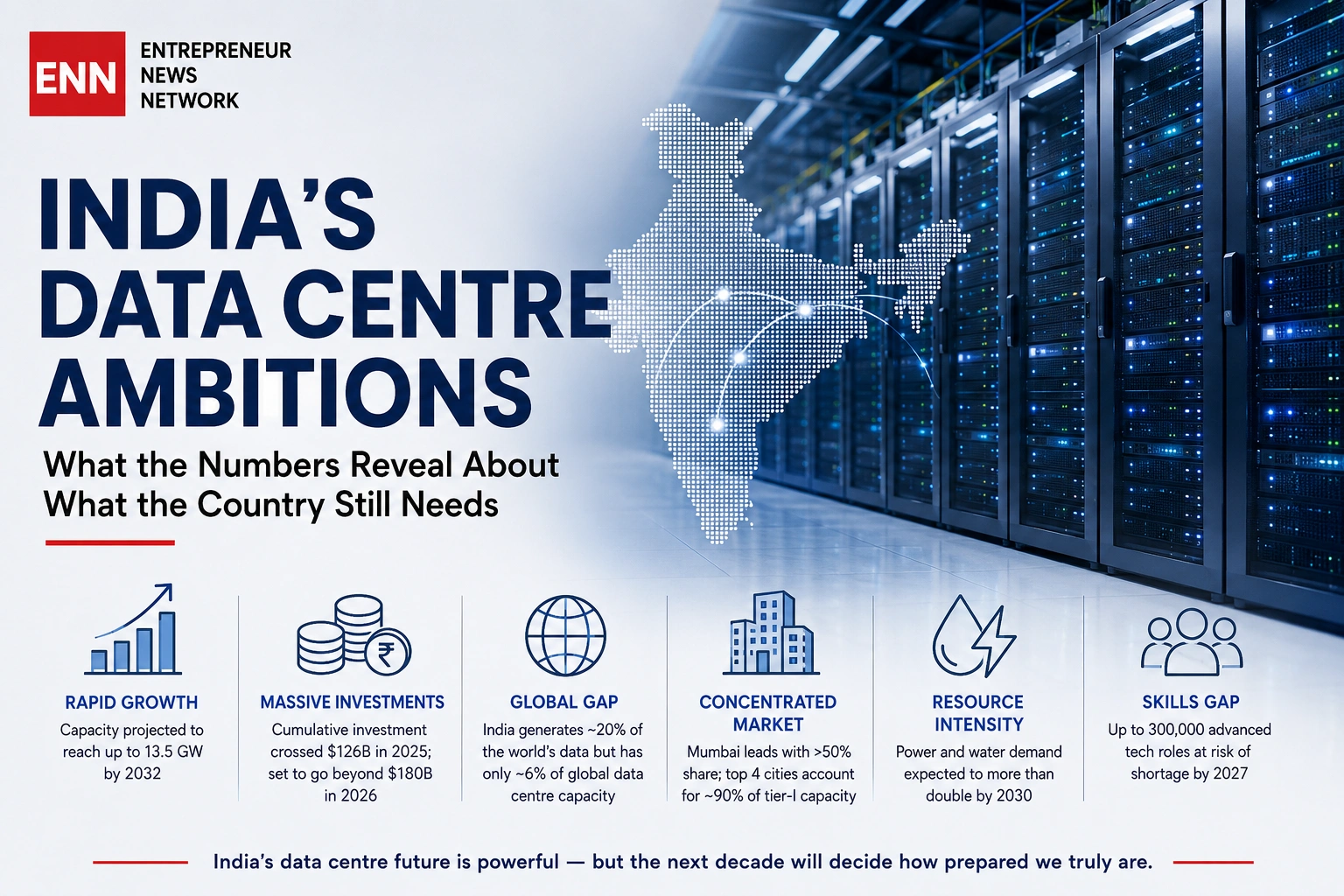

India wants to be a global data centre superpower, and on paper, the numbers back that ambition. The country’s installed data centre capacity crossed roughly 1,700 MW by the end of 2025, up from just 950 MW in 2024, and cumulative investment commitments in the sector hit $126 billion by the close of the same year, according to CBRE’s India Alternate Sectors Outlook 2026. Projections for 2026 push those figures even higher: CBRE expects total capacity to grow by around 30% year-on-year, adding roughly 500 MW of fresh supply, while cumulative investment commitments are forecast to surge by 45% to exceed $180 billion.

Those are extraordinary growth rates by any global standard. But growth rates alone don’t tell you whether a country is actually ready for the infrastructure it’s building. A closer look at India’s power grid, water resources, land availability, policy framework, and skilled workforce paints a more complicated picture — one where the ambition is real, but several structural gaps still need closing before the boom can be considered sustainable rather than simply large.

The Scale of India’s Data Centre Push, in Numbers

Before getting to what’s missing, it’s worth sitting with how fast this sector has actually grown. India added a record 440 MW of new data centre capacity in 2025 alone — a 160% jump over 2024’s additions — and various industry estimates put India’s installed IT load capacity at somewhere between 1.3 GW and 1.7 GW as of early 2026, depending on methodology. Real estate consultancy Vestian projects capacity will reach 1.7 to 2.0 GW by the end of 2026, backed by nearly $30 billion in investment, with the market scaling further to 4-5 GW by 2030.

More bullish, AI-accelerated scenarios cited by CBRE put India’s 2030 capacity range as high as 8 to 9.2 GW, with some long-range projections extending to 13.5 GW by 2032. To put that in perspective: India’s data centre capacity in 2020 stood at just 520 MW. Even the more conservative 2030 projections imply roughly a tenfold increase in a single decade.

Hyperscalers are driving a meaningful share of this. Microsoft, Amazon, and Google collectively pledged roughly $47.5 billion toward Indian data centre and AI infrastructure in commitments highlighted through late 2025, and Microsoft’s largest India facility is reportedly on track for a mid-2026 launch. The geographic centre of gravity is shifting too — while Mumbai has historically held close to half of India’s operational data centre inventory, rising land costs are pushing new hyperscale and AI-centric campuses toward Visakhapatnam and Hyderabad, in Andhra Pradesh and Telangana, which together are said to host over 2 GW of planned AI-focused capacity.

The Gap Nobody’s Headline Mentions: India Has 20% of the World’s Data, But Only 6% of Its Data Centre Capacity

Here is the number that should temper any sense that India’s data centre story is close to “done”: despite generating an estimated one-fifth of the world’s data, India holds only around 6% of global data centre capacity, according to figures cited by real estate firm Colliers. That mismatch is really the entire investment thesis behind the current boom — and it’s also a reminder of how much building still needs to happen before India’s digital infrastructure matches the scale of its digital economy, which is projected to contribute roughly 20% of national income by 2030.

As of January 2026, India hosted approximately 271 data centres occupying close to 23 million square metres of land, according to research from the Council on Energy, Environment and Water (CEEW) — a research and policy institution. For context, China and the United States together host thousands of facilities and account for a large majority of global data centre electricity consumption. India’s count of 271 still trails markets like Italy, Mexico, and Brazil in absolute facility numbers, even as its capacity-per-facility trends larger due to a hyperscaler-heavy mix — roughly a quarter of India’s data centre capacity is dedicated to hyperscale operators, per Savills research cited in CEEW’s analysis.

What India Needs 1: A Power Grid That Can Actually Carry the Load

Data centres are, at their core, industrial-scale electricity consumers, and this is where India’s ambitions meet their hardest constraint. CEEW’s research found that data centres accounted for around 0.5% of India’s national electricity consumption in 2024, alongside approximately 150 billion litres of annual water use — and both figures are projected to more than double by 2030.

The challenge isn’t simply generating enough electricity nationally; it’s delivering it reliably to specific high-density clusters. A single 100-MW hyperscale facility can require roughly 2 million litres of water per day for cooling, according to research compiled in a 2026 report on scaling India’s data centre ecosystem, and the concentrated, round-the-clock power draw of modern AI-focused facilities is straining local grids in ways that go beyond simple capacity addition. CEEW researchers have pointed specifically to transmission capacity bottlenecks, land acquisition challenges for renewable energy projects, and the lack of long-term power offtake agreements as constraints that could limit how much renewable energy can realistically be deployed near major data centre clusters.

The risk of getting this wrong has international precedent. Ireland’s data centre sector pushed electricity consumption to over 21% of national demand by 2023, prompting regulators to impose a moratorium on new data centre construction until 2028 specifically to protect climate targets. In the United States, data centres’ share of total electricity consumption rose from 1.4% in 2014 to 4.4% by 2023, a pace of growth that has already delayed coal plant retirements in some regions and pushed utilities toward new gas-based generation. India, where state electricity distribution companies are already financially stretched, has less room to absorb that kind of unplanned demand growth without consequences for grid stability or its own renewable energy transition.

What India Needs 2: A Real Answer on Water, Not Just Power

Power tends to dominate the data centre conversation, but water scarcity may be the more politically and environmentally sensitive constraint, particularly in a country where groundwater stress is already severe in many regions. Google alone reported consuming approximately 31 billion litres of water across all its global data centres in 2024 — a figure that illustrates the scale of the water question even before accounting for India-specific siting decisions.

The friction is already visible on the ground. In Andhra Pradesh’s Visakhapatnam district — among the regions positioning itself as a major AI-centric data centre hub — groundwater availability for domestic, agricultural, and industrial use stood at just 2.12 TMC (thousand million cubic feet) as of April 2026, among the lowest levels in the state, according to reporting by Mongabay India. State data centre policies in the region have proposed leveraging seawater cooling as an alternative, but the actual freshwater-to-seawater usage split for specific projects often remains undisclosed in public filings.

Compounding the problem is a regulatory gap: data centres currently have no separate category under India’s Environment Impact Assessment notification. They are typically classified as buildings or township development projects, which means many large facilities can obtain environmental clearance at the state level without a public hearing or a draft EIA report — a process that environmental researchers and civil society groups have flagged as insufficiently rigorous given the water and energy intensity of the facilities being approved.

What India Needs 3: Land Strategy Beyond the Big Four Metros

Mumbai, Chennai, Delhi-NCR, and Bengaluru together account for nearly 90% of India’s established tier-I data centre capacity, with Mumbai alone holding more than 50% of the country’s operational inventory as of the end of 2025, per CBRE’s data. That concentration made sense in the industry’s earlier phase, when proximity to subsea cable landing stations and existing fibre infrastructure mattered most. But it’s increasingly running into a hard constraint: land cost and availability in these four cities are rising fast enough to push new hyperscale development toward emerging hubs.

Tier-II cities including Ahmedabad, Visakhapatnam, Patna, Bhopal, Kochi, and Jaipur are seeing increased developer interest, driven by data localisation requirements, the ongoing 5G rollout, and lower land costs — but operational capacity in these markets is currently estimated at only 60-80 MW combined, a small fraction of the national total. Scaling these secondary markets will require more than developer appetite; it depends on whether state governments can deliver consistent power quality, faster permitting, and grid connections fast enough to match investor timelines, since power and permitting readiness vary far more in tier-II markets than in the established metros.

What India Needs 4: Policy Clarity That Goes Beyond Tax Breaks

India’s Union Budget 2026-27 introduced some of the most significant data centre-specific incentives the country has offered to date: a long-term tax holiday extending until 2047 for foreign cloud service providers using India-based infrastructure (contingent on using an Indian reseller for service delivery), a 15% safe harbour margin on costs for domestic data centres to reduce transfer pricing disputes, and proposed capital support of 25-35% for data centres investing in green technologies.

These measures matter, but policy analysts have cautioned that tax incentives alone won’t determine the sector’s trajectory. As one industry analysis put it, the real differentiator will be policy stability and seamless integration of renewable energy, not just tax breaks — a view echoed by the absence, as of early 2026, of a finalised, binding National Data Centre Policy. The policy remains in draft form, proposing tax incentives tied to capacity growth, energy efficiency, and employment generation, while national guidance on energy-efficiency best practices still largely traces back to a 2010 Bureau of Energy Efficiency compilation. In the meantime, state governments — including Andhra Pradesh, Telangana, Maharashtra, Tamil Nadu, Uttar Pradesh, Odisha, and Gujarat — have stepped in with their own competing data centre policies, creating a patchwork of incentive structures rather than one coherent national framework.

What India Needs 5: Enough Skilled People to Run What’s Being Built

Perhaps the least-discussed gap in India’s data centre story is workforce readiness. Industry estimates project a shortfall of 250,000 to 300,000 skilled professionals in adjacent semiconductor and advanced manufacturing roles by 2027, even though India produces roughly 600,000 electronics-related engineering graduates every year — only about 1% of whom currently possess the specialised capabilities needed for advanced fabrication, packaging, and precision equipment maintenance without significant retraining.

The data centre operations side faces its own version of this gap. The NIIT India Skills Gap Report 2026 found that 73% of core roles in monitoring and incident response at data centres are difficult to fill because the underlying technology — AI-driven monitoring tools, liquid-to-chip cooling systems required by high-density AI chips, and AIOps platforms — is evolving faster than academic curricula can track. As facilities shift from traditional air cooling toward liquid-based systems to handle the heat generated by modern AI chips, the talent required shifts too, from general facilities management toward specialists in thermal engineering and fluid dynamics — a category of expertise that barely existed in India’s data centre workforce a few years ago.

On the broader chip and electronics talent pipeline, the government has begun responding: the India Semiconductor Mission’s Chips to Startup (C2S) programme, launched in 2022 with a five-year outlay of ₹250 crore, aims to train 85,000 industry-ready semiconductor professionals, and Union Minister Ashwini Vaishnaw has stated the government’s ambition to scale semiconductor design training from 75,000 to 500,000 students. Whether that pace of skilling can keep up with the pace of capacity construction remains an open question — particularly because, unlike a data hall or a substation, trained talent cannot be built on a fixed construction timeline.

The Bottom Line: Execution, Not Ambition, Is the Constraint

Every figure in India’s data centre story — 1,700 MW of capacity, $126 billion in cumulative commitments, a projected $180 billion by the end of 2026 — points toward extraordinary momentum. But the more revealing numbers are the ones describing what’s not yet in place: a national data centre policy still in draft form, an EIA framework with no dedicated category for the sector, water-stressed regions hosting some of the most ambitious AI-campus plans, and a skills pipeline that, by multiple independent estimates, is not yet producing enough specialised talent to staff the facilities already under construction.

None of this means India’s data centre ambitions are overstated. The country genuinely holds a disproportionately small share of global capacity relative to the data it generates, and the capital is clearly willing to flow toward closing that gap. What the evidence suggests instead is that India’s data centre boom has moved past the “will the investment come” question and into a harder one: whether power, water, land-use planning, policy, and workforce development can be scaled with the same urgency as the capital commitments themselves. As CEEW’s researchers put it, the decisions India makes now on siting, power sourcing, and cooling technology will lock in land, energy, and water impacts for decades — making this less a story about data centres, and more a story about whether the country’s underlying infrastructure planning is ready for the digital economy it is trying to build.

Sources: CBRE India Alternate Sectors Outlook 2026; Council on Energy, Environment and Water (CEEW); Vestian; Colliers; India Brand Equity Foundation (IBEF); Mongabay India; Policy Circle; CSIS; NIIT India Skills Gap Report 2026.

Henkel Appoints Pradhyumna Ingle as India Country President to Accelerate Growth and Innovation

Ruchi Kumar is the associate editor at Entrepreneur News Network and TVW News India, where she leads editorial strategy, brand storytelling, and startup ecosystem coverage. With a strong focus on innovation, business, and marketing insights, he curates impactful narratives that spotlight India’s evolving entrepreneurial landscape. She has written extensively on fintech, AI and emerging startups.